Tech Tactics

As nations vie for supremacy in critical and emerging technologies, geopolitics and high-tech innovations intersect to shape global dynamics. Technological advances, from artificial intelligence to space exploration, not only revolutionise industries but redefine global power and strategic alliances as well. This edition explores the newly signed US-Taiwan high-tech trade agreement; how China is scrutinising the Manus-AI sale to US’s Meta, a high-tech supply chain chokepoint in the global automotive industry; how Special Economic Zones (SEZ) and tech parks aren’t silver bullets for attracting high-tech investment; and the need for India to route its profitable corporattions’ cash into Research and Development (R&D).

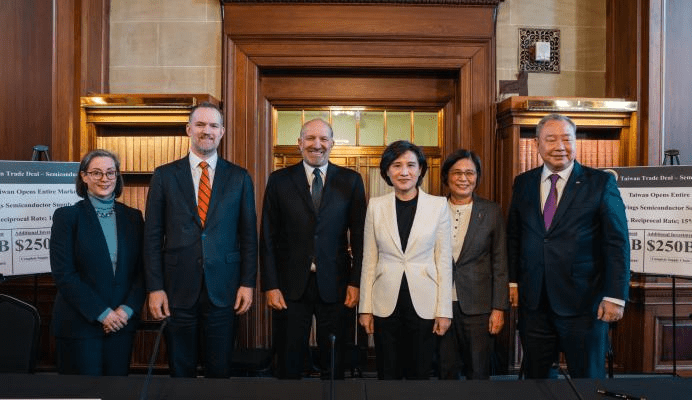

Taiwan consolidates high-tech trade partnership with US

Taiwan is positioning itself to deepen its technological alignment with the United States (US), using artificial intelligence (AI) and advanced semiconductors as the centrepiece of a broader economic and strategic recalibration. A Memorandum of Understanding (MoU) was signedon 15 January 2026 with Washington, which was formalised on 12 February 2026, lowering tariffs on a wide range of Taiwanese exports while committing the island’s companies to new direct investments of about US$ 250 billion across the US technology ecosystem.

The agreement reflects sustained pressure from the Trump administration for greater onshore production of chips that underpin AI systems, data centres and next-generation computing. Taiwan sits at the heart of these supply chains, supplying a large share of the world’s most advanced semiconductors. Washington’s objective is not simply to secure supply, but to embed a larger portion of that capability within US borders.

Under the deal, Taiwanese firms are expected to direct up to US$ 250 billion into the US over time, spanning semiconductors, AI infrastructure and energy-related technologies. This includes roughly US$ 100 billion that has already been announced by Taiwan Semiconductor Manufacturing Company (TSMC) for new capacity and expansion projects. Parallely, Taiwan will provide credit guarantees of a similar scale to support further outward investment by its companies.

For Taipei, the strategy is framed as an expansion rather than a relocation of its technology base. Taiwanese officials have stressed that investment decisions will remain company led and driven by market demand, with domestic production continuing alongside overseas growth. The intent is to extend Taiwan’s industrial footprint into the US while reinforcing its role as a central node in global technology supply chains.

The deal also carries political weight. The US remains Taiwan’s most important security partner despite the absence of formal diplomatic ties. By anchoring cooperation in AI and semiconductors, both sides are reinforcing an economic relationship that has increasingly strategic overtones. This comes at the risk of aggravating Beijing, which claims Taiwan as its territory and opposes high-level engagement between Taipei and Washington.

From Washington’s perspective, the agreement advances two goals at once. It accelerates the build-out of domestic semiconductor and AI capacity, and it reduces reliance on production concentrated in East Asia. US officials have indicated that failure to localise supply chains could trigger punitive tariffs, signalling that market access is now explicitly tied to investment location.

Lawmakers have raised concerns that excessive overseas investment could weaken Taiwan’s own manufacturing base, particularly in advanced nodes that underpin its economic and strategic relevance.

Taiwanese authorities have pushed back against this narrative, arguing that diversification strengthens resilience rather than hollowing out capacity. Current projections suggest that the bulk of advanced chip production will remain on the island well into the next decade, even as US capacity grows. According to them, spreading production across geographies reduces systemic risk without undermining Taiwan’s technological leadership.

The semiconductor sector is central to this balancing act. TSMC, the dominant global producer of advanced logic chips, has reiterated that its expansion plans are guided by customer demand, particularly from US-based AI and cloud computing firms. Demand for cutting-edge process technology remains strong, and the company continues to invest heavily at home while expanding abroad.

Beyond chips, the investment programme extends into AI servers, data centre infrastructure and energy systems needed to support hyper-scale computing. These areas tie Taiwan more closely into the US-led AI build-out, where most large-scale deployments and capital spending are expected to occur.

Taiwan has also made certain purchase commitments including US$ 44.4 billion worth of liquefied natural gas and crude oil; US$ 15.2 billion worth of civil aircraft and engines; and US$ 25.2 billion worth of power equipment, power grids, materials, generators, storage facilities, marine equipment, steel-making equipment and other equipment from 2025 through 2029.

Once ratified by Taiwan’s legislature, the agreement will mark one of the largest outward investment pushes by a US partner economy. It underscores how trade, technology and geopolitics are becoming increasingly intertwined. For Taiwan, the challenge will be maintaining its position as an indispensable technology hub while adapting to a world where access to markets is increasingly conditional on where critical capabilities are built.

China hits back: Beijing is scrutinising Manus-AI’s sale to Meta for brain drain concerns

Meta Platforms’s acquisition of Manus-AI, a Singapore-based AI startup with strong Chinese connections, has triggered a robust regulatory response from Beijing. Valued at over US$ 2.5 billion and finalised in late 2025, the deal aims to integrate advanced AI agents that can handle complex, multi-stage workflows—such as research, data analysis, and coding—into Meta’s consumer and business products. However, it now faces a formal probe by China’s Ministry of Commerce for potential breaches of technology export controls. Beijing views the transaction as a conduit for exporting sensitive AI algorithms and expertise, prompting swift intervention to protect its national interests.

Manus originated in China under the company Butterfly Effect and was marketed as a general-purpose AI agent for autonomous tasks. Amid US investment curbs and domestic challenges, the company shifted to Singapore in mid-2025, securing US$ 75 million from US Venture Capital (VC) firm Benchmark while cutting China-based roles and closing local social media presence. A proposed Alibaba partnership for a China-tailored version didn’t pan out, redirecting focus to Western markets.

This relocation strategy, often termed “Singapore washing” whereby Chinese-linked entities shift to Singapore which is a far more amenable jurisdiction politically in the eyes of US authorities, enabled the Meta buyout. Yet Chinese authorities maintain that Manus retains ties to its mainland parent entities, founders, and talent. Under China’s export rules, interactive AI systems qualify as dual use technologies requiring approval, similar to precedents in deals involving TikTok.

Manus likely employs many engineers who were trained under or with funding from China’s top academic aid programmes such as Tsinghua’s AI labs and the Thousand Talents Programme, embodying talent honed in state-supported ecosystems. Their transfer to Meta could spark a talent exodus, undermining China’s lead in generative AI during escalating US-China tech tensions.

The Chinese government is likely to intervene in any major high-tech relocation that it doesn’t fully orchestrate for its own means, potentially imposing technology transfer limits or blocking the deal outright to discourage emulation or Intellectual Property (IP) theft. Beijing takes the same approach to foreign firms with Chinese IP holdings or origins. The review process by regulators began in December, to look into possible national security implications, people familiar with the matter said. The deal will be assessed for its consistency with relevant laws and regulations, Ministry of Commerce spokesman said at a regular briefing. The Financial Times first reported review, which is in its early stages and regulators might ultimately choose not to intervene, the people said, asking to remain anonymous discussing a sensitive situation. In some cases, reviews of this kind can become formal probes and — if violations are alleged — potentially result in penalties or a demand for certain conditions before deal approval.

As of February 2026, Meta is integrating the acquisition of Manus into its ecosystem, while the startup faces a regulatory review in China over technology export controls. Despite the acquisition, Manus is expanding its service, launching agents on Telegram in February 2026, even while Meta faces scrutiny for allegedly restricting other AI on WhatsApp. While some users expressed data privacy concerns following the Meta acquisition, others have continued to use the service for its high-level, multi-agent task automation, which includes coding and workflow management.

Single points of failure: Exploring the phenomena of over-dependence on single-origin component design

Nexperia’s Dongguan facility in Guangdong Province of China, is a high-volume node for discrete diodes, small signal transistors, and basic logic chips integral to automotive electronic control units (ECUs) used in cars for lighting, power management, and advanced driver assistance systems (ADAS). Owing to its large order book from automakers across the world, the facility also became a global chokepoint for the industry in late 2025.

The production taxonomy of even legacy semiconductor nodes reveals inherent vulnerabilities, even for old ubiquitous chips; wafer fabrication occurs in European hubs while packaging, testing, and binning is concentrated in China’s cost effective ecosystem with specialised backend tooling and rapid throughput. By mid-2025, this geographic skew rendered global automotive networks hypersensitive to localised disruptions, whether operational outages or calibrated export restraints.

The Dutch government’s intervention in November 2025, invoking national security and briefly taking over Nexperia’s corporate structures under the European Union’s (EU) Foreign Investment Screening Regulation triggered Beijing’s retaliatory export curbs on Nexperia’s mainland China output, severing guaranteed flows of the product. At that time, the situation deteriorated to the point that reliable multi-sector component manufacturers and subassembly suppliers like Bosch and Continental issued force majeure notices, while original equipment manufacturers (OEMs) including Nissan, Mercedes-Benz, and Honda signalled production curtailments. The European Automobile Manufacturers’s Association (ACEA) projected module shortages cascading to assembly halts, with Honda already idling lines in Wuhan, and North American plants echoing COVID19 pandemic era pauses.

This episode exposes a transactional paradigm in automotive manufacturing supply chains which are riddled with cost cutting, high volumes, low-margin components sourced via just-in-time consolidation despite the ever looming chance of shortages, all in the name of optimisation and capital efficiency. Seemingly, despite lessons learned from the COVID-era shutdowns and supply chain disruptions, all the vows of developing redundancies and establishing alternative supply sources have largely evaporated, leaving single points of failure across supply and value chains.

This episode exposes a transactional paradigm in automotive manufacturing supply chains which are riddled with cost cutting, high volumes, low-margin components sourced via just-in-time consolidation despite the ever looming chance of shortages, all in the name of optimisation and capital efficiency. Seemingly, despite lessons learned from the COVID-era shutdowns and supply chain disruptions, all the vows of developing redundancies and establishing alternative supply sources have largely evaporated, leaving single points of failure across supply and value chains.

The most obvious solution is to institutionalise redundancy rather than dedicate all resources to transactional operations. Global precedents also affirm this approach. Taiwan diversified its chip ecosystem by fusing TSMC’s fabrication facilities with packaging and testing facilities in Singapore and Malaysia. Similarly, Japan’s government mandated dual sourcing after the Fukushima Daiichi nuclear power plant disaster.

Counting your elephants before they fly: Structural deficits in SEZs, tech parks, and industrial corridors undermine high-tech investment

India has operationalised 276 special economic zones (SEZs), numerous tech parks, and billions worth of industrial corridors since the early 2000s, yet these have catalysed greenfield investment predominantly in low-barrier assembly rather than in high-tech fabrication. This shortfall stems not from insufficient scale or incentives, but from foundational design misalignments that prioritise relocation speed over technological embedding.

SEZs such as Noida Export Processing Zone in the National Capital Region (NCR), Mumbai’s Santacruz Electronics Export Processing Zone (SEEPZ), and Tamil Nadu’s Sriperumbudur electronics cluster excel in export-oriented assembly, testing, and packaging for sectors like mobile devices, medical instruments, and automotive components.

Incentives by the Central and state governments, including 100% income tax exemptions for five years and single window customs clearance, are aimed towards minimising setup friction for activities reliant on imported capital goods and a highly valuable skilled workforce.

High-tech sectors such as semiconductor fabrication, giga factory scale battery production, and precision optics demand multi-year process tuning, indigenous supplier ecosystems, and iterative Research & Development (R&D) production loops, rendering SEZ rebates insufficient against these inherent disadvantages. Consequently, multinational firms limit SEZs in the Global South, including India, to downstream value capture while retaining core IP and piloting upstream in home bases in already heavily clustered Taiwan or South Korea.

Tech parks exhibit an even starker divergence. Bengaluru’s Electronic City, Hyderabad’s HITEC City, and Pune’s Hinjewadi clusters have scaled software services and backoffice engineering to global leadership, employing millions of professionals, yet they are home to few indigenous hardware or deep tech firms. The lack of shared infrastructure such as pilot fabrication facilities, materials characterisation labs, cleanroom certification suites, and accelerated life testing bays, lead firms to face prohibitive standalone costs.

Industrial corridors for their part do amplify logistics but falter on capability genesis. The Delhi-Mumbai Industrial Corridor (DMIC), spanning 1,504 km and with 24 planned nodes, has attracted automotive forging, warehousing, and petrochemicals via dedicated freight corridors and 24×7 power grids. The Chennai-Bengaluru Industrial Corridor (CBIC) reinforces electronics assembly around the Foxconn and Samsung plants. Neither has spawned self-reinforcing high-tech clusters, as they sideline technology de-risking, specialised skilling, and mission aligned procurement.

While not counterproductive to the goal of attracting and enabling investments, tech parks, corridors, and SEZs need to be seen as incentive disbursement mechanisms and not silver bullets that can answer India’s complex and multifaceted problems in the digital industrial age.

Capital misallocation demands a high-tech fund and mandated R&D beyond incubators

India’s high-tech ascent hinges not on ideation as is evident from the burgeoning IIT patent pipelines and startup density, but on capital at the scale-up stage where platform technologies demand sustained, high-risk deployment backed by fiscal liquidity.

India’s IT majors, despite generating hundreds of billions of dollars in annual export revenues, largely channel their surpluses into service-line expansion, overseas acquisitions, and incremental automation. In contrast, their R&D intensity remains a small fraction of revenues when compared with similarly profitable multinational firms. Client-specific customisation continues to take precedence over the development of proprietary platforms, resulting in IP retention constraints.

While incubators and incentive programmes, such as Atal Innovation Mission hubs and SIDBI seed schemes, are of some value in advancing proof-of-concept ventures, they are unable to provide the scale of funding required for capital intensive needs such as pilot production lines, validation rigs, and first-customer trials. Banks generally avoid lending to deep-tech ventures that are not backed by adequate collateral, and domestic venture capital firms likewise seek more certainty than their counterparts in the US and China.

A sovereign high-tech capital fund, capitalised at US$ 20-30 billion through budgetary allocation and public sector undertaking (PSU) surpluses, could be designed to address this gap. The fund would take equity positions in semiconductor pilot fabrication facilities, shared battery giga factories, precision tooling ecosystems, and biotech scale-up infrastructure. Established through statute, it would mandate co-investment from private corporates and reduce risk through government offtake guarantees, akin to India’s solar Production Linked Incentive (PLI) programme.

Complementing this approach, a legislated R&D spending requirement, modelled on the Corporate Social Responsibility (CSR) mandate of 2% of profits, would internalise spending on R&D within firms. Companies could meet this obligation by utilising captive laboratories at national facilities such as IIT Madras’s semiconductor centre, or through sector-calibrated financial contributions. Together, these mechanisms would generate demand signals for innovation and curbs passive cash hoarding, a pattern that has unfortunately characterised many Indian mid-cap and large-cap firms with substantial foreign remittance inflows.

Check these out:

Apergis, E., Markoulakis, A., & Apergis, N. (2025). ‘The semiconductors–economic growth nexus’. International Journal of the Economics of Business, 32(3), xxx–xxx.

Bloomberg News. (2026, January 7). China reviews Meta’s $2 billion deal to buy AI startup Manus.

Ezell, S. (2024, February 14). Assessing India’s readiness to assume a greater role in global semiconductor value chains. Information Technology & Innovation Foundation.

Blackwell, H. (2026, February 16). United States and Taiwan sign agreement on reciprocal trade. International Trade Insights; posted in ‘International Trade & Supply Chain, International Trade Remedies, Tariffs & Trade Policy’.

Inside Micron Taiwan’s semiconductor factory | Taiwan’s mega factories EP1. (n.d.). YouTube video.

Pantheon Insights. (2025, May 12). US–China AI bifurcation: The new tech iron curtain (Part I).

Pantheon Insights. (2025, May 12). US–China AI bifurcation: The new tech iron curtain (Part I).

The Hindu. (n.d.). Why have special economic zones rules been relaxed? | Explained.

Tobin, M., Chang Chien, A., & Wu, X. (2026, January 15). Taiwan reaches trade deal with Trump, pledges more U.S. chip factories. The New York Times.